Thinking about crypto exchange in Korea options this year? You’ve got more choices than ever—local KRW on-ramps with real-name bank accounts, non-custodial swappers for quick coin-to-coin moves, and pro-grade platforms for secure crypto trading Korea. The key is to stay on the right side of Korea’s user-protection rules, compare fees realistically, and pick the workflow that fits how you buy/sell or how to swap crypto in Korea.

Why Choose Local Exchanges?

Benefits of Domestic Services

Korean platforms plug directly into the banking system, which means fast crypto exchange Korea experiences: KRW deposits/withdrawals via linked real-name bank accounts and a smoother compliance process than overseas sites. The “real-name” framework has been a bedrock of Korea’s crypto policy since 2018—banks issue exchange-linked accounts to verified users, and anonymous deposits are not permitted. That improves traceability and reduces fraud risk for everyday buy/sell crypto flows.

Regulatory Compliance

Two pillars shape operations in 2025:

- Anti-money-laundering/VASP registration. Under the Act on Reporting and Using Specified Financial Transaction Information, all virtual-asset service providers (VASPs) that target Korean users must register with KoFIU and meet requirements like ISMS security certification and Travel Rule compliance.

- Virtual Asset User Protection Act (in force since July 19, 2024). This law requires segregation of client assets, bank custody of KRW deposits (with interest), insurance/reserve arrangements for hacks, market-abuse surveillance, and empowers regulators to sanction rule-breakers. It also warns consumers about risks from OTC/P2P deals outside supervised venues.

Good to know: Korea postponed crypto capital-gains tax again—no crypto gains tax until January 2027, per late-2024 parliamentary actions. Plan ahead, but the enforcement clock isn’t running in 2025.

Top Crypto Exchanges in South Korea

This isn’t financial advice; always verify a platform’s KoFIU registration and current bank partner before you deposit.

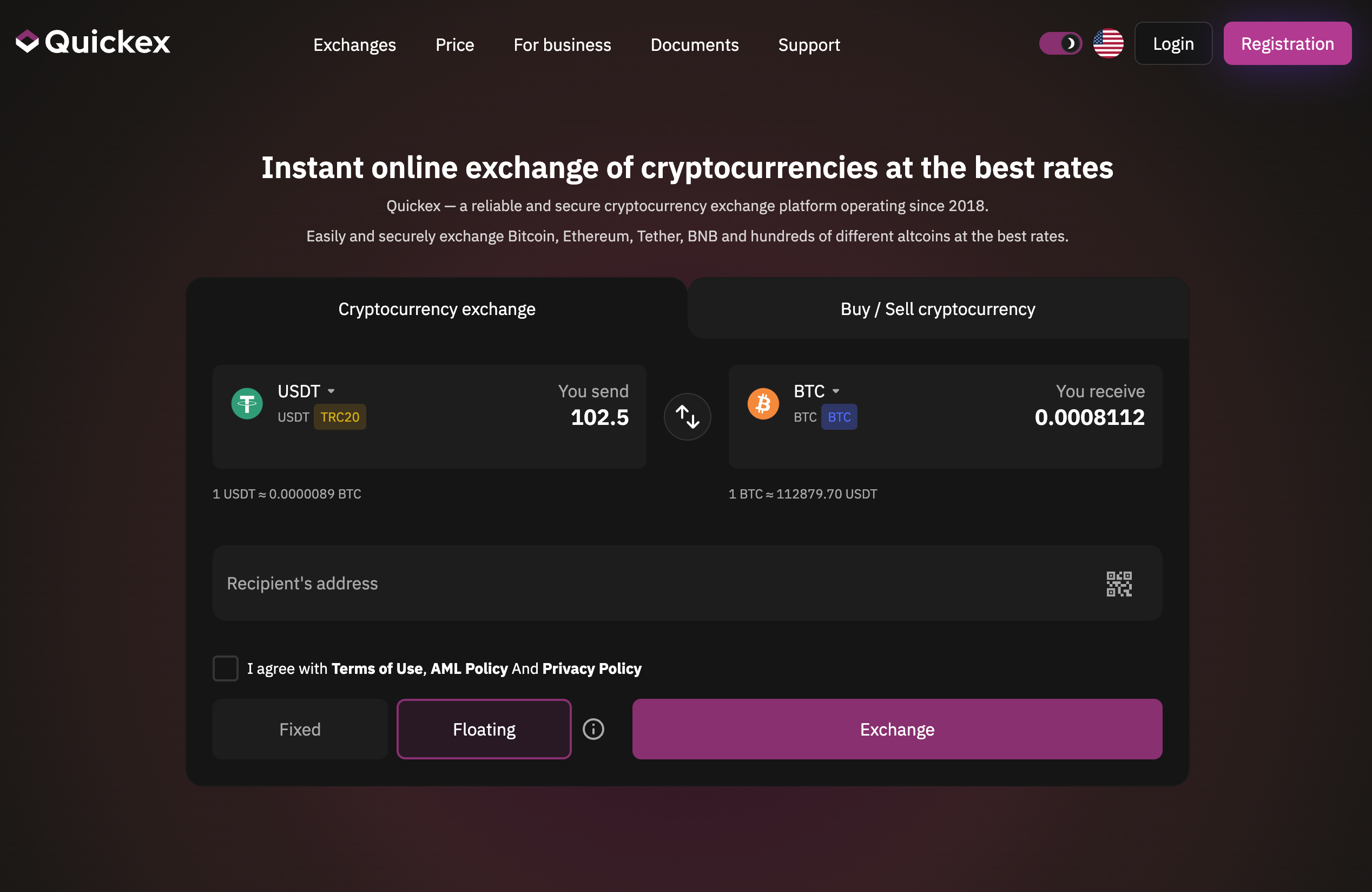

Quickex Overview

Quickex.io is a CEX instant swapper—ideal when you want to convert one coin to another (e.g., exchange BTC to ETH) without parking funds on an exchange. You just paste a receiving address, confirm a quote, send crypto, and receive to your wallet.

Upbit Overview

Upbit is Korea’s largest venue by volume and users, widely seen as the market’s liquidity hub. Recent reports place its domestic market share ~73%, thanks to deep KRW order books and strong brand recognition. Upbit’s banking partner is K-Bank (internet-only bank), enabling real-name KRW rails.

Bithumb Overview

Bithumb remains Korea’s #2 heavyweight. In early 2025, it struck a new real-name account partnership with KB Kookmin Bank, one of Korea’s big four—an important shift that could enhance Bithumb’s competitiveness against Upbit.

Features, Fees, and Limits

- KRW deposits/withdrawals: enabled via real-name bank accounts tied to each exchange. Banks vet exchanges and users—expect strict KYC.

- Trading fees: maker/taker schedules differ per venue; “convert” buttons are simpler but may add spread.

- Listing & monitoring: under the 2024 user-protection law, exchanges maintain surveillance systems and stricter token-listing standards; DAXA (industry SRO) publishes best-practice guidelines.

Step-by-Step Guide to Exchanging Crypto

Supported Payment Methods

- KRW bank transfer (real-name account): the mainstream route for fiat to crypto exchange Korea. Link the exact bank partner the exchange uses; deposits/withdrawals are typically fast during banking hours.

- Card rails: less common for KRW on local exchanges due to chargeback risk and costs; check each venue’s policy.

- Coin-to-coin swaps: use Quickex or the exchange’s spot markets to rotate between assets without touching KRW.

Using Wallets and P2P Platforms

- Self-custody first: set up a reputable wallet (hardware or audited mobile). For crypto wallet support Korea, bank-linked exchanges plus wallets like Ledger/Trezor or audited mobile options cover most needs.

- P2P/OTC caution: The FSC explicitly warns that OTC and P2P markets lack proper surveillance. If you do engage, use escrow, stick to verified counterparties, and keep complete records of transfers and receipts. For most people, supervised exchanges are the safer default.

Clean KRW workflow:

Create account → complete KYC → open/verify real-name bank account link → deposit KRW → buy/sell → withdraw KRW back to your bank or withdraw coins to self-custody.

Security and Legal Considerations

- Law in force: The Virtual Asset User Protection Act (effective July 19, 2024) mandates segregation of customer assets, KRW deposits held at banks (with interest), insurance/reserves against hacks, and surveillance/reporting of unfair trading (e.g., manipulation). The FSS/FSC can inspect and sanction VASPs.

- AML/KoFIU registration: If a foreign platform targets Korean users, registration is required; unregistered services risk enforcement and must cease Korea-facing business.

- Travel Rule & reporting: Korea enforces the Travel Rule for VASPs alongside ISMS certification; expect enhanced verification on withdrawals to external wallets and to other exchanges.

- Tax timing: Parliament pushed crypto capital-gains taxation to 2027. Keep meticulous records anyway; rules can evolve and you’ll want clean cost basis/history. (Consult a local tax professional.)

Alternative Methods for Crypto Exchange

- Non-custodial swappers: Great for instant crypto swap use-cases (e.g., rotating BTC→ETH or consolidating altcoins). Not a KRW on-ramp—pair it with a local exchange if you need KRW cash-out.

- International exchanges (non-KRW): May offer broader listings and derivatives for eligible users, but if they target Korean users without KoFIU registration, they’re offside. When in doubt, stick to where to exchange crypto Korea options that are clearly registered.

- OTC desks: Corporate or HNW trades sometimes use bank-vetted OTC, but expect rigorous compliance checks under the user-protection act and AML regime.

Tips to Save on Fees and Time

- Use KRW bank transfers on your exchange’s designated partner bank—cheaper and cleaner than card rails.

- Mind spreads vs. fees: “Convert” buttons are simple but may cost more than limit orders on the order book.

- Test sends for on-chain moves: When withdrawing coins, send a small test first; exchanges often cannot recover funds sent to the wrong network or without required memos (applies to some assets).

- Watch lending/staking rules: Korea is tightening guardrails on yield/lending products (e.g., interest caps, over-collateralization rules) to protect users—read platform notices before you participate.

- Avoid unregistered platforms/P2P scams: The regulator’s consumer note is clear—unsupervised OTC/P2P lacks market surveillance. Stick to supervised rails unless you fully understand the risks.

Conclusion

For everyday users, the safest path to crypto trading Korea is straightforward: pick a KoFIU-registered exchange with a real-name bank partner, fund via KRW transfer, and trade with transparent fees and clear audit trails. If you only need coin-to-coin speed, a non-custodial swapper like Quickex is handy—just remember it’s not a KRW off-ramp. And if you’re comparing platforms, focus on liquidity, banking convenience, fee schedules, and how well the venue implements Korea’s user-protection law.

Thanks to robust oversight (and the 2024 act now in force), secure crypto trading Korea is more predictable in 2025. Keep good records (tax kicks in 2027), treat P2P as advanced, and use the checklist above to find the best crypto exchangers in Korea for your needs—whether your priority is cheap crypto exchange Korea, fast on-ramps, or rock-solid compliance.

FAQ — Crypto Exchange Korea

What wallets do Koreans use for crypto and payments?

South Koreans use two distinct layers of digital wallets: everyday payment wallets (Naver Pay, Kakao Pay, Toss, Samsung Pay) and crypto-specific wallets — with domestic exchange wallets, MetaMask, Trust Wallet, and the Korean-built D’CENT hardware wallet being the most popular.

Everyday payment wallets

Four players — Naver Pay, Kakao Pay, Toss Pay, and Samsung Pay — have become central to how consumers pay and interact with banks in Korea. In 2025, an estimated 98% of South Koreans use digital wallets in some form. In 2024, over 75% of online purchases happened on mobile devices, and platforms like Naver Pay, Kakao Pay, Toss, and Samsung Pay have become a normal part of daily life. Samsung Pay now enables tap-to-pay functionality for Naver Pay and Kakao Pay users, significantly expanding offline usability. The major players in the industry are Kakao Corporation, Naver Financial Co., Ltd, Samsung Electronics Co. Ltd, Toss Payments Co., Ltd, NHN Payco Co., Ltd, and Coupang, Inc.

Crypto wallets popular in South Korea

Most Korean crypto users hold their assets on domestic exchange wallets (Upbit, Bithumb, Coinone, Korbit) due to the real-name bank account requirement. For self-custody, Koreans have access to the same global wallet ecosystem:

- MetaMask — MetaMask serves over 30 million monthly active users and 143 million lifetime downloads, placing it second in CoinGecko’s 2026 hot-wallet ranking behind Trust Wallet. Widely used among Korean DeFi and NFT users on Ethereum and EVM chains.

- Trust Wallet — Trust Wallet supports 100+ blockchains, powered by infrastructure capable of supporting 130+ networks natively with $0 fees on staking, buying, sending, and receiving — the most downloaded self-custody wallet globally with 220 million+ users.

- D’CENT Wallet (Korean-made) — D’CENT Wallet is a crypto wallet company launched by South Korean cybersecurity firm IoTrust in 2018. As of 2026, D’CENT has more than 700,000 users worldwide, making it one of the most popular hardware wallet providers on the planet. The Biometric Wallet was the world’s first biometric-secured hardware wallet when it launched.

Summary table:

| Category | Wallet | Type | Key Feature |

|---|---|---|---|

| Payments | Naver Pay | Mobile payment | Dominant in online commerce |

| Payments | Kakao Pay | Mobile payment | Integrated with KakaoTalk messenger |

| Payments | Toss | Mobile payment / neobank | Stocks, payments, banking in one app |

| Payments | Samsung Pay | Mobile payment | NFC tap-to-pay, widest offline coverage |

| Crypto (exchange) | Upbit Wallet | Custodial (exchange) | Largest KRW trading volume |

| Crypto (self-custody) | MetaMask | Hot wallet (browser + mobile) | #1 Web3/DeFi wallet, EVM focus |

| Crypto (self-custody) | Trust Wallet | Hot wallet (mobile-first) | 100+ chains, 220M+ global users |

| Crypto (hardware) | D’CENT | Cold wallet (biometric) | Korean-made, fingerprint security, 4,500+ coins |

| Crypto (hardware) | Ledger | Cold wallet | Global standard, 8M+ devices sold |

What is the D’CENT wallet — and why is it popular in Korea?

D’CENT is a biometric hardware wallet built by the South Korean cybersecurity firm IoTrust. It’s the country’s most prominent homegrown crypto wallet and the world’s first cold wallet with fingerprint authentication.

D’CENT Wallet is developed by IoTrust, a South Korea-based security firm founded in 2017 by ex-Samsung engineers. It launched the world’s first biometric hardware wallet in 2018 and now serves 700K+ users worldwide. IoTrust’s backers include top Korean VCs, including Korea Investment Partners (KIP), KB Investment, and Korea Development Bank Capital.

Key features of D’CENT:

- Biometric security: The D’CENT Biometric Wallet uses a certified secure CC EAL5+ chip, the gold standard for digital security among hardware wallet manufacturers.

- Broad asset support: D’CENT Wallet supports more than 4,500 cryptocurrencies across more than 85 blockchains.

- Multi-wallet management: In 2025, the wallet introduced multi-wallet support to allow users to create up to 100 app wallet accounts within a single interface.

- GasPass (fee-less transactions): D’CENT introduced GasPass earlier in 2025, a feature that allows users to experience fee-less onchain transactions. As long as you have GasPass, D’CENT will pay transaction fees conducted on blockchains such as Ethereum, Base, and Solana. This lets users send transactions and interact with dApps without needing to hold native tokens for fees, making onboarding smoother for newcomers.

- Card Wallet option: In addition to its primary biometric device, D’CENT also offers a Card Wallet. This wallet, which costs just $38, is a credit-card-sized device that uses Near Field Communication (NFC) technology to enable mobile crypto transactions.

- Non-custodial design: D’CENT Wallet is a fully non-custodial wallet provider, meaning that the company has no access to users’ private keys.

D’CENT’s popularity in Korea stems from a combination of local brand trust (Korean-founded, Korean VC-backed, Korean-language support), hardware-grade security familiar to Samsung-centric consumers, and a mobile-first ecosystem that fits Korea’s smartphone-dominant culture.

What are the top crypto exchanges in South Korea in 2026?

South Korea has one of the world’s most regulated and active crypto markets, dominated by five FSC-registered domestic exchanges with KRW banking partnerships — plus global platforms used by Korean traders.

South Korea is one of the world’s most active digital asset markets. Domestic trading is shaped by high retail participation, KRW order books, strict bank-linked real-name accounts, the Travel Rule, and the well-known Kimchi Premium. To legally accept Korean won (KRW) deposits, exchanges must obtain VASP registration with the FIU and demonstrate they hold a real-name account agreement with a domestic bank. As of early 2026, only five exchanges hold verified partnerships: Upbit (K-Bank), Bithumb (KB Kookmin Bank), Coinone (Kakao Bank), Korbit (Shinhan Bank), and Gopax (Jeonbuk Bank).

The “Big Five” domestic exchanges:

| Exchange | Bank Partner | Key Strength |

|---|---|---|

| Upbit | K-Bank | Largest KRW volume, 150+ KRW pairs, 98% cold storage |

| Bithumb | KB Kookmin Bank | 200+ coins, margin & futures, 8M+ users |

| Coinone | Kakao Bank | First Korean blockchain remittance app (“Cross”) |

| Korbit | Shinhan Bank | Korea’s first exchange (2013), strong beginner focus |

| Gopax | Jeonbuk Bank | Binance-linked liquidity since 2023 |

Global platforms popular with Korean traders:

The best crypto exchanges in South Korea in 2026 include Upbit, Bithumb, Korbit, Binance, Bybit, Coinone, Bitget, and MEXC. While globally headquartered, KuCoin has built a significant user base in South Korea. Its intuitive design, vast token listings, and competitive fees make it one of the most popular global exchanges used by Korean traders.

Regulation update: South Korea’s crypto gains tax for individuals remains unimplemented as of March 2026, delayed three times with a potential fourth push to 2027 or later. The Income Tax Act imposes 22% on annual crypto income over 2.5M KRW (~$1,750), far below the 50M KRW stock threshold, sparking trader backlash.

Can foreigners use Korean crypto exchanges — and what are the restrictions?

Foreigners residing in Korea can use domestic exchanges, but they face the same strict KYC requirements as Korean citizens — including a real-name Korean bank account, which is the main barrier.

Foreigners residing in Korea can use Korean crypto exchanges, but they must comply with the same regulations as Korean citizens, including real-name verification through a Korean bank account. KRW-based platforms need banking relationships that match users’ verified identities. This is why domestic platforms often require a matching bank account, resident registration or foreign registration details, phone verification, and strict onboarding checks.

What this means in practice:

- For residents with a Korean bank account: You can register on Upbit, Bithumb, Coinone, Korbit, or Gopax using your Alien Registration Card (ARC) and matching bank account. The onboarding process mirrors what Korean nationals go through.

- For tourists, short-term visitors, or non-residents: Domestic KRW exchanges are effectively inaccessible. Without a Korean bank account linked to a verified real-name identity, you cannot deposit KRW or trade on regulated platforms.

- The alternative — global exchanges and no-KYC swaps: Non-residents can use global platforms like Binance, Bybit, or KuCoin (crypto-to-crypto only, no KRW). For the fastest option with no registration at all, Quickex lets you swap any supported cryptocurrency without an account — just select a pair, enter your wallet address, and send coins.

These regulatory layers combine with strict KYC and AML obligations to create a walled garden: excellent liquidity for Korean residents, near-total inaccessibility for everyone else.

How can I swap crypto in South Korea without KYC — and is Quickex available?

Yes — Quickex is available globally, including South Korea. It allows you to swap crypto instantly without registration, KYC, or a Korean bank account.

The crypto wallet market in South Korea is expected to reach a projected revenue of US$ 5,703.1 million by 2033. A compound annual growth rate of 28.4% is expected from 2026 to 2033. With this rapidly expanding market, Korean users increasingly seek flexible, privacy-respecting tools for crypto conversion — especially for cross-border swaps and assets not listed on domestic KRW exchanges.

How to swap crypto via Quickex — step by step:

- Go to quickex.io and select your trading pair — for example, BTC → USDT, ETH → XRP, SOL → USDC, or any of 500+ supported coins.

- Enter the amount — the aggregator scans multiple liquidity providers and shows you the best available rate. Choose a fixed rate (guaranteed output) or a floating rate (follows the market at execution).

- Paste your recipient wallet address — double-check the address and network. Blockchain transactions are irreversible.

- Send your coins to the unique deposit address generated for your order.

- Receive your coins — once confirmed on-chain, Quickex automatically converts and delivers the target asset to your wallet.

Why Quickex fits the Korean market:

- No Korean bank account needed — swap crypto-to-crypto without KRW banking restrictions.

- No registration or KYC — just your wallet address. No personal data stored.

- Non-custodial — Quickex never holds your funds beyond the swap execution window.

- 500+ coins supported — including assets not always listed on Korean domestic exchanges.

- Fixed and floating rates — choose the option that fits your risk preference.

- Average swap time: 5–10 minutes.

Whether you’re a Korean resident looking to swap tokens not available on Upbit, a foreigner without a Korean bank account, or simply someone who values privacy — Quickex offers a fast, secure, and straightforward alternative.