Diving into the world of decentralized finance, or DeFi, can feel like unlocking a new level in a video game – exciting, but you need the right tools to play smart. That’s where Compound Finance comes in, flipping the script on traditional banking by automating crypto lending and borrowing. It seemed too good to be true, letting anyone earn interest on their holdings or grab a loan without begging a bank. But here we are in 2025, and it’s still a powerhouse in space. This guide breaks down what Compound Finance is all about, how it pulls off that automation magic, the nuts and bolts of getting involved, and some real-talk on the risks. Whether you’re a newbie eyeing your first deposit or a seasoned trader, stick around – we’ll make sense of it all.

Getting the Basics: What is Compound Finance?

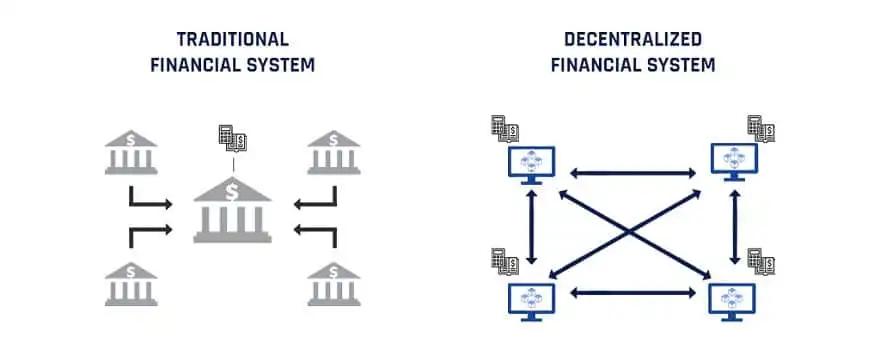

At its heart, Compound Finance is a DeFi protocol built on Ethereum ecosystem and other chains like Base and Arbitrum. It’s all about creating an open marketplace where folks can lend out their crypto assets to earn interest or borrow against what they own, all without middlemen. No credit checks, no paperwork – just smart contracts handling everything automatically. The compound finance definition boils down to an algorithmic system that adjusts interest rates based on supply and demand in real-time. If more people want to borrow a certain token, rates go up; if lenders flood the market, they dip.

Launched way back in 2018, it’s evolved a ton. By 2025, with updates like the Compound Growth Program roadmap, it’s supporting more assets and tighter governance. The COMP token plays a big role here, letting holders vote on changes. Think of it as a community-run bank, but digital and borderless. Unlike old-school finance where your savings gather dust at fixed rates, here everything compounds – interest on interest, growing your stack over time.

Why does this matter in crypto? Well, traditional banks lock up your money with low yields, while crypto’s volatile nature means you might want quick access. Compound bridges that, turning idle assets into earners.

Key Features at a Glance: A Quick Comparison Table

To wrap your head around what sets Compound apart, here’s a table highlighting its core elements versus traditional lending. It shows how automation changes the game.

| Aspect | Compound Finance | Traditional Banking |

| Interest Calculation | Algorithmic, real-time based on market dynamics | Fixed or variable, set by bank policies |

| Access Requirements | Wallet connection, no KYC for basic use | ID verification, credit score checks |

| Collateral | Over-collateralized crypto assets | Often unsecured or asset-backed with appraisals |

| Speed | Instant deposits/withdrawals via blockchain | Days for approvals and transfers |

| Governance | COMP token holders vote on proposals | Centralized decisions by executives |

| Risks | Smart contract vulnerabilities, liquidation | Default risks, but insured deposits |

This setup underscores the efficiency – no waiting around for approvals. Recent 2025 proposals, like adding weETH as collateral, keep expanding options.

The Inner Workings: Automating Lending on Compound

Lending on Compound is straightforward once you grasp the flow. You supply assets to a pool, and borrowers dip in, paying interest that flows back to you. The protocol uses cTokens – like cETH for Ethereum – as receipts for your deposit. These earn compound interest automatically, minted when you lend and redeemable anytime.

Automation shines through algorithms that tweak rates. For instance, if USDC demand spikes, borrow rates climb to attract more lenders. It’s supply-demand economics on steroids, all coded in. In 2025, with upgrades to Governor contracts, the system’s more resilient against hacks or glitches. I’ve lent small amounts myself and watched the balance tick up without lifting a finger – that’s the beauty of compound finance crypto.

Borrowing flips it: You lock up collateral, say 150% of what you want to borrow, to cover volatility. If prices drop too far, liquidation bots step in automatically, selling off to repay. No human oversight needed, which cuts costs but amps risks.

Step-by-Step: How Do I Connect to Compound Finance?

Ready to jump in? Connecting is easier than setting up a new app on your phone. Here’s a marked list of steps to get you started – I’ve followed them plenty of times.

- Grab a Compatible Wallet: Use something like MetaMask or WalletConnect. Load it with ETH for gas fees.

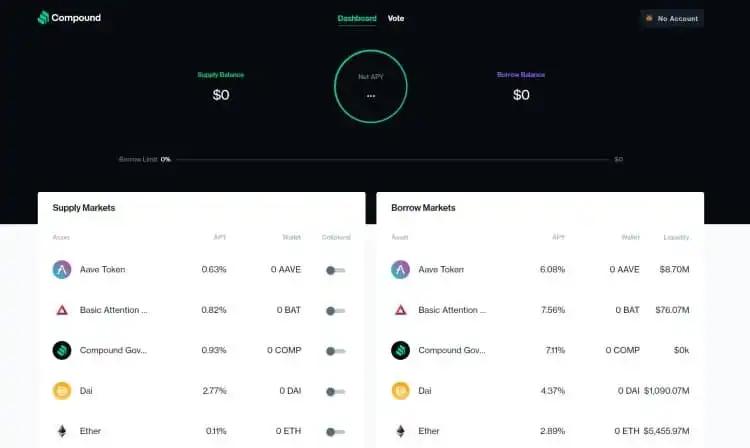

- Head to the Site: Visit app.compound.finance. It’s the main dashboard for interactions.

- Connect Your Wallet: Click “Connect” and approve in your wallet app. No sign-up needed beyond that.

- Choose an Asset: Pick from supported ones like ETH, USDC, or newer additions like sdeUSD. Check current rates.

- Supply or Borrow: For lending, approve and deposit. For borrowing, supply collateral first, then take out the loan.

- Monitor and Manage: Use the app to track interest, adjust positions, or withdraw. Set alerts for liquidation thresholds.

Once connected, everything runs on autopilot. If you’re funding your wallet, services like Quickex come in handy. This exchanger streamlines fiat-to-crypto swaps with low fees and fast execution, supporting tons of pairs – perfect for topping up before hitting Compound without delays.

Diving Deeper: Borrowing Mechanics and Risks

Borrowing isn’t free money – it’s leveraged play. You over-collateralize to borrow, say putting up $150 in ETH to get $100 in DAI. Interest accrues on the borrow, compounded block by block. The utilization rate drives this: High borrowing means higher rates to balance pools.

But watch out – liquidation is the big bad wolf. If your collateral dips below a factor (like 125%), the system sells it off, slapping a penalty. In volatile markets, this happens fast. Plus, smart contract risks: Though audited, bugs could drain funds. Governance attacks have hit DeFi before, but Compound’s COMP holders keep voting on fixes, like the 2025 security provider engagement.

On the flip, rewards in COMP tokens incentivize participation, distributed based on activity. It’s a way to earn extra while lending or borrowing.

Why It Matters: The Impact on Crypto Ecosystems

Compound’s automation democratizes finance, letting anyone from anywhere join. No borders, no biases – just code. In 2025, with multi-chain support, it’s integrating with L2s for cheaper fees, making it accessible even in high-gas times. Compound fi, as some call it shorthand, has inspired copycats, but its governance model sets the bar.

For lenders, it’s passive income; for borrowers, quick capital without selling assets. Imagine holding Bitcoin long-term while borrowing against it for real-world spends – that’s the power.

Potential Drawbacks and Tips for Safe Play

No system’s perfect. Beyond liquidations, there’s impermanent loss if pools shift, or oracle failures messing rates. Always diversify – don’t dump everything into one asset.

Tips: Start small, use tools like DeFi dashboards for monitoring, and keep an eye on governance proposals via tally.xyz. In 2025, the renewed Governance Working Group ensures smoother operations.

Wrapping Up: Your Path Forward with Compound

Compound Finance has automated crypto lending and borrowing into something approachable, turning complex finance into a few clicks. From its algorithmic roots to 2025 enhancements like expanded collaterals, it’s a staple for DeFi enthusiasts. Whether earning on stablecoins or leveraging alts, the key is understanding the automation – it works for you, but respect the risks. If you’re intrigued, connect today and see the compound magic firsthand. Who knows, it might just compound your portfolio in ways you didn’t expect.