In digital asset markets, the number displayed on a trading screen is not a fixed truth but a transitory consensus. In short, the crypto exchange rate represents the most recent price at which two parties agreed to transact a pair of assets (for example, ETH/USDT). As with any exchange rate in traditional finance, that figure shifts continuously in response to order flow, liquidity conditions, information arrival, and broader macroeconomic forces. This article explains how prices are formed on centralized and decentralized exchanges, why quotes may differ across platforms, how liquidity and slippage affect realized outcomes, and what practical steps improve trade execution.

Price formation on centralized and decentralized Exchanges

On centralized exchanges, matching engines pair bids and offers from an order book. Market orders consume the best available rates and, when size exceeds visible depth, progress through multiple price levels, creating slippage. Limit orders, by contrast, restrict execution to a specified price or better, at the risk of remaining unfilled. The resulting crypto exchange rate is therefore a function of resting liquidity and immediate demand.

On decentralized exchanges, automated market makers (AMMs) quote prices algorithmically from token reserves held in liquidity pools. Large orders push the pool along a pricing curve, so the effective price depends on pool depth as well as the trade’s size. Concentrated-liquidity designs can tighten spreads near the prevailing level but may widen rapidly if liquidity providers withdraw or shift their ranges.

Read more here: Centralized vs Decentralized: Differences in Crypto Exchanges

Why quotes differ across platforms

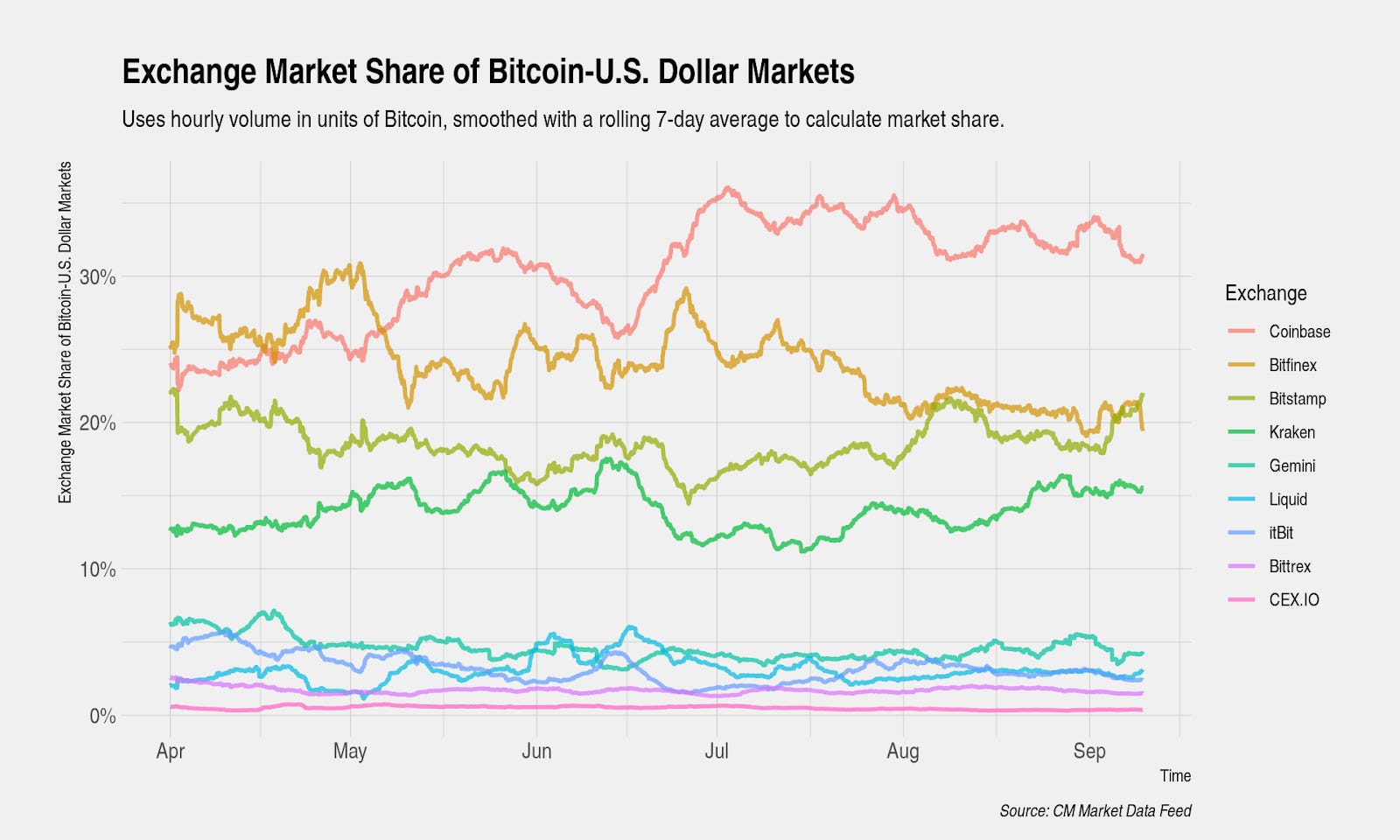

Cryptocurrency trading is fragmented across numerous centralized venues, rollups, and AMM pools. Because connectivity, latency, and depth vary, the observed crypto exchange rate may diverge across platforms at any given instant. Arbitrageurs normally compress these gaps by buying where prices are lower and selling where they are higher. However, during periods of network congestion, risk reduction, or constrained capital, dislocations can persist longer, allowing spreads between venues to remain elevated.

Liquidity, slippage, and execution quality

Liquidity describes the capacity to transact size with minimal price impact. When depth is thin, even moderate orders can move markets materially. Market participants therefore monitor top-of-book size, aggregate depth at relevant price intervals, and pool reserves on AMMs. Slippage controls—maximum tolerable deviation from the quoted BTC price—protect against adverse fills but may cause transactions to fail when set too strictly. The same mechanics apply to redemptions: attempting to exit through a narrow venue often results in inferior execution relative to the headline quote.

The role of stablecoins

Stablecoins frequently serve as a settlement asset in crypto pairs, providing speed and broad acceptance without requiring fiat rails at the point of trade. For instance, many traders exchange BTC to USDT to standardize balances or to move between venues. Stability, however, depends on collateral quality, disclosure practices, and redemption frameworks. Under stress, a token can trade at a premium or discount to its reference currency, introducing a minor basis between the token pair and the corresponding fiat pair.

News, information, and episodic volatility

Source: Coinmetrics

Prices adjust when market participants update expectations. Protocol upgrades, security incidents, regulatory actions, and fund-flow data are common catalysts. In order-book markets, liquidity providers widen or withdraw quotes until uncertainty resolves; in AMMs, arbitrage moves pools toward the new consensus level. The immediate print may therefore vary across venues based on connectivity, risk appetite, and the speed at which each market integrates new information.

Macro influences and fiat foreign exchange

Digital assets trade not only against each other but also against major currencies. Consequently, movements in the dollar, euro, or yen affect crypto-fiat pairs through the familiar channel of the exchange rate. Interest-rate expectations, inflation data, and changes in risk sentiment all influence the cost of capital and investors’ willingness to hold volatile assets. Derivatives markets transmit these conditions back to spot via funding rates and basis, shaping both trend and intraday dynamics.

Why the same trade can yield different outcomes

Two traders pursuing identical ideas can experience distinct results. Consider a purchase executed into a thin AMM pool during a period of elevated gas fees versus a staged sequence of limit orders on a deep centralized book outside peak hours. The first trader accepts material slippage and higher transaction costs; the second reduces impact and cost by pacing orders and selecting a deeper venue. Routing, timing, and order type often matter as much as direction.

A concise model for understanding price behavior

A useful framework is to view the observed crypto exchange rate as the product of three forces:

- Microstructure: order-book depth, spreads, and AMM pool size determine the mechanical sensitivity of price to a given order.

- Cross-venue alignment: arbitrage reduces discrepancies but may be limited by capital, risk constraints, or technical frictions.

- Information and macro: new data and broader financial conditions set the destination toward which prices converge, while microstructure defines the path.

Practical steps for better execution

- Select the appropriate venue. For larger transactions, prioritize exchanges with deep books or AMMs with ample reserves; consider aggregators that source multiple pools.

- Use order types judiciously. Limit orders define acceptable prices; market orders prioritize immediacy. Time-weighted or laddered strategies can reduce impact.

- Monitor conditions. Spreads and depth deteriorate around major announcements; schedule discretionary trades when markets are more stable.

- Assess settlement currency. If trading against a tokenized cash leg, be mindful of small premiums or discounts relative to fiat.

- Test and verify. When you exchange crypto on a new venue or chain, send a small transaction first to validate routing, fees, and settlement speed.

- Compare routes. When available, use tools that simulate alternative paths and display all-in costs, including fees and network charges.

Summary

The exchange rate visible on a trading interface is a continuously updated agreement, shaped by market microstructure, arbitrage, information flow, and macroeconomic context. Centralized order books and decentralized AMMs arrive at prices through different mechanics, yet both are sensitive to liquidity and order size. Quotes vary across venues because the market is fragmented and because capital, technology, and risk tolerances differ. By understanding these drivers—venue selection, order type, timing, settlement asset quality, and cost components—market participants can improve execution quality and align realized results more closely with displayed prices.

In short, the number on the screen is not merely a label; it is the outcome of many moving parts. Recognizing how those parts interact equips traders and investors to navigate volatility more effectively and to reduce avoidable costs when interacting with the exchange rate that governs each transaction.

FAQ: Crypto Exchange Rates, Fees & Best Platforms

What fees do crypto exchanges charge?

Crypto exchange fees come in several layers — understanding all of them is critical, because the advertised “trading fee” is often just a fraction of the real cost.

- Trading fee (maker/taker): Charged on every buy or sell order. “Maker” = limit order that adds liquidity (lower fee). “Taker” = market order that removes liquidity (higher fee). Typical range: 0.10% – 0.60% on major exchanges.

- Spread: The hidden difference between the buy and sell price offered by the exchange. Some platforms (Coinbase Simple, Crypto.com App) embed a 0.5–2.0% spread on top of the trading fee, making the real cost significantly higher than advertised.

- Deposit fee (fiat): Bank transfer is usually free; credit/debit card deposits cost 2–5% due to payment processor fees.

- Withdrawal fee (crypto): Charged when you move crypto off the exchange to your wallet. This covers the network fee (gas) and sometimes includes the exchange’s markup. Examples: BTC withdrawal ~0.0001–0.0005 BTC; ETH withdrawal ~0.001–0.005 ETH; USDT TRC-20 ~$1.

- Withdrawal fee (fiat): Depends on method — ACH free, SEPA free or €0.15, wire $5–$35, Faster Payments free.

- Conversion fee: Some platforms charge a separate fee for instant buy/sell or “convert” features (distinct from spot trading). Coinbase Simple charges up to 3.99% on card purchases.

- Inactivity fee: Rare in 2026, but some exchanges charge monthly fees on dormant accounts. Kraken, Coinbase, and Binance do not charge inactivity fees.

How to minimise total fees:

- Use the exchange’s advanced/pro trading interface (Coinbase Advanced Trade, Kraken Pro) — not the simplified “buy” button, which has 3–10× higher fees.

- Deposit via bank transfer (free) instead of credit/debit card (2–5%).

- For crypto-to-crypto swaps, use QuickEx — ~0.5–1% all-in fee with no hidden spread, no account, and no withdrawal fee (output goes directly to your wallet).

What is the best crypto exchange with the lowest fees?

The lowest fee crypto exchange depends on what type of trade you’re making. Here’s a direct comparison of real total costs across the top platforms in 2026:

| Exchange | Maker Fee | Taker Fee | Card Purchase | Hidden Spread | KYC |

|---|---|---|---|---|---|

| Binance | 0.10% | 0.10% | ~1.8% | None (spot) | ✅ Yes |

| Kraken Pro | 0.16% | 0.26% | ~3.75% | None (pro) | ✅ Yes |

| Coinbase Advanced | 0.40% | 0.60% | ~3.99% | ~0.5% (simple app) | ✅ Yes |

| Gemini ActiveTrader | 0.20% | 0.40% | ~3.49% | ~0.5% (simple app) | ✅ Yes |

| Bybit | 0.10% | 0.10% | ~2.5% | None (spot) | ✅ Yes |

| QuickEx | ~0.5–1% all-in (swap) | N/A | Rate shown before confirmation | ❌ No | |

- Lowest spot trading fee (with KYC): Binance — 0.10% maker/taker, the global benchmark. Available worldwide except certain US restrictions.

- Lowest US-regulated fee: Kraken Pro — 0.16%/0.26%, available in all 50 states, strong compliance track record.

- Lowest no-KYC fee: QuickEx — ~0.5–1% all-in for crypto-to-crypto swaps with no account, no ID, and no withdrawal fee. The rate you see before confirming is the rate you get.

- Beware “simple buy” fees: Coinbase’s simple app charges up to 3.99% on card purchases vs. 0.60% on Advanced Trade. Always use the pro/advanced interface.

What is the most trusted crypto exchange in the USA?

Trust in a US crypto exchange is determined by regulatory compliance, security track record, insurance coverage, and years of incident-free operation. Here’s how the top US-regulated exchanges compare on trust in 2026:

| Exchange | Regulatory Status | Security Record | Insurance / Custody | Trust Score |

|---|---|---|---|---|

| Coinbase | Publicly traded (NASDAQ: COIN), registered MSB, NY BitLicense, 50-state coverage | No major hack in 12+ years; 2021 SMS phishing incident affected ~6,000 accounts (reimbursed) | $255M+ FDIC-insured USD balances; crypto held in cold storage with Coinbase Custody (SOC 1 & SOC 2) | ⭐⭐⭐⭐⭐ |

| Kraken | FinCEN MSB, FINTRAC (Canada), FCA (UK), available in all 50 US states | Zero major security breaches since founding (2011); regular proof-of-reserves audits | Industry-leading cold storage protocols; no FDIC insurance on USD but strong operational security | ⭐⭐⭐⭐⭐ |

| Gemini | NY Trust Company (NYDFS chartered), SOC 2 Type 2 certified, available in all 50 states | No major hack; Gemini Earn controversy (2022–2023) involved partner Genesis, not Gemini exchange assets | SOC 2 audited; FDIC-insured USD; Gemini Custody with $200M insurance on crypto assets | ⭐⭐⭐⭐½ |

Industry security breaches: 2024–2025 context

- No major US exchange was hacked in 2024–2025. The largest crypto incidents during this period affected DeFi protocols and bridges, not regulated US CEXs.

- FTX collapse (2022) remains the defining event — it was neither US-regulated nor properly audited. This disaster accelerated US regulatory enforcement and raised the bar for proof-of-reserves and custody standards.

- WazirX hack (July 2024): $235M stolen — affected an Indian exchange, not US platforms.

- DMM Bitcoin hack (May 2024): $305M stolen — affected a Japanese exchange.

- Lesson: US-regulated exchanges (Coinbase, Kraken, Gemini) have the strongest security track records in the industry. If you prioritise trust above all else, stick to these three.

- Most trusted overall: Coinbase — publicly traded, NASDAQ-listed, 12+ year security record, broadest US regulatory coverage, FDIC-insured USD.

- Best security purist: Kraken — zero breaches since 2011, proof-of-reserves leader, lowest fees among top-3 US exchanges.

- Best institutional trust: Gemini — NYDFS Trust Company charter, SOC 2 Type 2 audit, $200M custody insurance.

What crypto exchanges accept credit cards?

Most major crypto exchanges accept credit cards in 2026, but card-based purchases are the most expensive way to buy crypto due to payment processor fees. Here’s the full picture:

| Exchange | Credit Card | Debit Card | Card Fee | KYC |

|---|---|---|---|---|

| Coinbase | ✅ Visa, Mastercard | ✅ Visa, Mastercard | 3.99% | ✅ Yes |

| Kraken | ✅ Visa, Mastercard | ✅ Visa, Mastercard | ~3.75% | ✅ Yes |

| Binance | ✅ Visa, Mastercard | ✅ Visa, Mastercard | ~1.8–2% | ✅ Yes |

| Gemini | ✅ (via debit only in some regions) | ✅ Visa, Mastercard | ~3.49% | ✅ Yes |

| Crypto.com | ✅ Visa, Mastercard | ✅ Visa, Mastercard | ~2.99% | ✅ Yes |

| Bybit | ✅ Visa, Mastercard | ✅ Visa, Mastercard | ~2–3% | ✅ Yes |

- Cheapest card purchase: Binance — ~1.8% for Visa/Mastercard, the lowest among major exchanges.

- Additional card costs to watch:

- Many banks treat crypto card purchases as a cash advance, adding a 3–5% cash advance fee + immediate interest accrual (no grace period). Check with your bank first.

- Visa and Mastercard may apply a foreign transaction fee (1–3%) if the exchange is domiciled outside your country.

- Cheapest alternative: Buy crypto with a bank transfer (ACH, SEPA — typically free) instead of a card. If you already hold any crypto, swap on QuickEx — zero card fees, no KYC, ~0.5–1% all-in.

What is the best crypto exchange in the USA?

The best crypto exchange in the USA depends on your priority — lowest fees, most trusted, widest coin selection, or best for beginners. Here’s the definitive ranking by use case:

- Best for beginners: Coinbase — simplest UX, broadest US regulatory coverage (NASDAQ-listed), educational content, staking, and the most intuitive mobile app. Higher fees on the simple app (use Advanced Trade for 0.40–0.60%).

- Best for low fees: Kraken Pro — 0.16% maker / 0.26% taker, available in all 50 states, strong security record since 2011. Best fee/trust ratio in the US market.

- Best for institutional / compliance: Gemini — NYDFS Trust Company charter, SOC 2 Type 2 certified, $200M custody insurance, IRA accounts via Gemini Custody. Higher fees (0.20%/0.40%) but maximum regulatory coverage.

- Best for altcoins: Coinbase (200+ assets) or Kraken (200+ assets) — the widest selection among fully US-regulated exchanges. For 500+ coins including privacy coins and niche altcoins, use QuickEx (crypto-to-crypto swap, no KYC).

- Best for no-KYC: QuickEx — swap any of 500+ coins without registration, ID, or account. Not a US-regulated exchange, but non-custodial (no funds held). Ideal for privacy-conscious US users who already hold crypto and want to swap.

How to swap crypto on QuickEx and get the best exchange rate?

QuickEx shows you the exact exchange rate before you confirm — no hidden spread, no post-trade surprises. Here’s how to swap and ensure you get the best rate:

- Go to QuickEx.io — no account, no email, no KYC required.

- Select your exchange pair — e.g. BTC → ETH, USDT → SOL, LTC → BTC, ETH → XMR, or any of 500+ supported combinations.

- Enter the amount and choose your rate type:

- Fixed rate — the output amount is locked at the moment you confirm. You receive exactly what was quoted, regardless of price movement during the swap. Best for volatile markets or large amounts.

- Floating rate — the output tracks the live market rate until the swap is executed. Slightly lower fee than fixed rate, but the final amount may differ ±1–2% from the initial quote. Best for stable markets or when you want the absolute lowest fee.

- Review the rate — QuickEx displays:

- Exchange rate (e.g. 1 BTC = 27.43 ETH)

- Estimated output amount

- Network fee included in the rate

- Estimated arrival time

- Paste your destination wallet address — the wallet where you want to receive the output coin.

- Send your crypto to the QuickEx deposit address shown on screen.

- Receive your coin directly in your wallet — typically within 5–30 minutes depending on network confirmation times. No funds are ever held by QuickEx.