Market attention is fixed on the Federal Reserve’s October meeting. It’s not so much the likelihood of a rate cut. Investors are worried about how confidently the regulator can act while effectively flying blind. Because of the ongoing U.S. government shutdown, the central bank has to decide without key economic data.

Here’s the backdrop the Fed brings into decision day—and how the changes could affect the crypto market.

Track how the Bitcoin price reacts to Fed decisions with Quickex.

A cut is a foregone conclusion

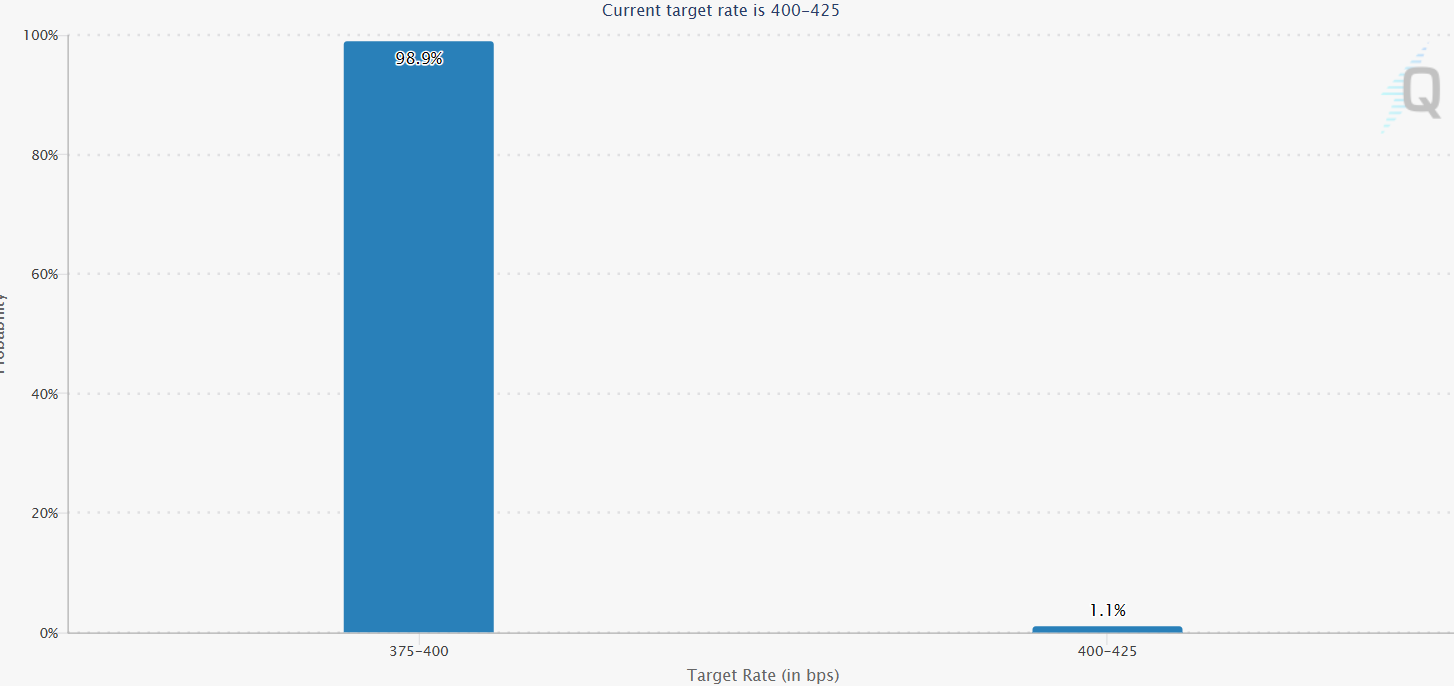

The Federal Open Market Committee meets on October 28–29, and markets put the odds of a 0.25 percentage point cut at nearly 100%. That would lower the federal funds range to 3.75–4.00%.

Forecast of the Fed’s rate decision on October 29. Source: CME

The reason is obvious—labor market cooling. By private estimates, from June to August average job gains slowed to around 30,000 per month, noticeably below the pre-pandemic pace. In September the Fed already made its first cut of the year, and most analysts see October as a logical continuation of the easing path.

The Fed’s internal balance: caution vs. decisiveness

Christopher Waller and Michelle Bowman advocate a moderate cut. Steven Miran, a new Board member appointed by Donald Trump, proposes cutting by 0.5 pp at once, arguing the current level is too high. Alberto Musalem of the St. Louis Fed said he’s ready to support another cut in October unless inflation risks intensify.

Fed Chair Jerome Powell has essentially signaled readiness to step down. At the same time, he avoids making calls about December. And Kansas City Fed President Jeffrey Schmid is confident today’s rates are still sufficiently restrictive to restrain price growth.

The overall mood: move carefully, meeting by meeting, until data confirm a sustained slowdown in inflation and hiring.

The main problem—shutdown and a “data vacuum”

Today the Fed is operating almost blind. Since October 1, federal agencies have suspended publication of crucial reports—above all on employment and consumer spending. The last full Bureau of Labor Statistics report came out back in early September.

As Nomura economist David Seyf noted, officials are simply “flying blind.” Without fresh data, any assessment of the economy turns into guesswork.

Alternative sources—private employment trackers, jobless claims, bank transaction data—only partly compensate for the loss of official statistics. Thomas Barkin, president of the Richmond Fed (one of the Fed’s 12 regional banks), explained that credit-card data are useful, but they don’t cover people without cards—and that’s about a quarter of the population.

As a result, the Fed can’t tell whether the slowdown is driven by weaker demand or by labor shortages due to limited immigration. That directly affects how to interpret soft job gains—and which policy to choose next.

September CPI: a rare glimmer of data

By order of the Trump administration, part of the Labor Department’s staff returned to work to publish the September Consumer Price Index (CPI) on October 24—needed to adjust Social Security benefits.

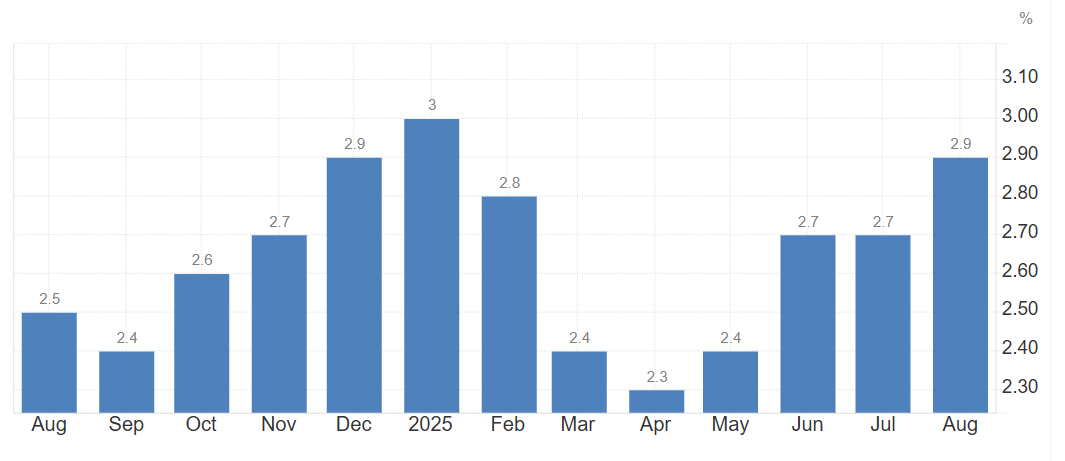

Reuters economists expect inflation to come in around 3.1% year over year, a bit above prior readings. That will keep tensions within the Fed: some see price growth as a signal for caution, others view it as manageable and compatible with gradual easing.

U.S. inflation data. Source: tradingeconomics

The core PCE (personal consumption expenditures price index), the Fed’s preferred gauge, reached 2.7% in August and, by forecasts, could touch 3.0% by year-end, then start to decline in 2026. However, rising household expectations for persistent price increases worry some FOMC members: if people get used to higher inflation, bringing it back to the 2% target becomes harder.

When will the shutdown end: five critical dates

The shutdown has already become one of the three longest in U.S. history, and there are no signs Congress and the White House are close to a deal. The economic damage grows by the day, and the following dates could be turning points:

October 24 — federal employees miss a full paycheck for the first time. More than two million families will face financial pressure, reducing consumption and hurting local businesses.

October 31 — the next payday for the military. The administration already found $8 billion in reserves to fund the October 15 payroll, but lawmakers say repeating that by month-end is unlikely.

October 31 and November 5 — paydays for congressional staff. Many workers risk going unpaid, adding to lawmakers’ own frustration.

November 1 — the start of open enrollment under Obamacare. This is a key sticking point: Democrats want to maintain subsidies, Republicans oppose them.

Thanksgiving week (November 21–28) — if the shutdown lasts into this period, the country could face a transport crunch: air-traffic controllers and TSA staff would work without pay, and mass “sick-outs” could snarl flights, as happened in 2019.

The closer we get to November, the stronger the pressure on politicians. But negotiations are still at a standstill.

How the shutdown hampers the economy and Fed decisions

According to Reuters, the Federal Reserve itself remains financially independent and continues to collect information through its regional surveys. These show consumer spending weakening, while business investment is growing mainly on the back of surging interest in artificial intelligence.

Even so, the lack of official statistics makes forecasts imprecise and reduces policymakers’ confidence in their actions.

Minneapolis Fed President Neel Kashkari acknowledged:

“We’re managing for now, but the longer the shutdown drags on, the less confident we are that we understand the true state of the economy.”

Looking ahead: December—the key moment of the year

The Fed’s September projections revealed a wide dispersion of views. Some members expect two more cuts; others think it’s time to pause. That’s why the December 9–10 meeting will be pivotal.

By then, the Fed will have accumulated data following the shutdown, updated its forecasts, and—for the first time in months—been able to gauge the real trajectory of inflation and employment. That’s when it will become clear whether the easing cycle continues.

What this means for crypto

For cryptocurrencies, the Fed-plus-shutdown story is a double-edged sword. On one side, if the rate is indeed cut, the dollar may soften a bit and risk appetite may rise. In such episodes investors often return to crypto: Bitcoin and Ethereum tend to climb, pulling others along.

But the shutdown complicates everything. Because of it, the Fed is almost guessing—no data, no confidence. If inflation suddenly accelerates, the regulator could hit pause in December, and markets would cool instantly.

So crypto is trading on expectations. An October cut could deliver a brief pop, but until the government reopens and the outlook clears, the crypto market will keep oscillating between cautious optimism and fear of a fresh wave of uncertainty.

Bottom line

An October 0.25 pp cut is almost inevitable. What happens next depends on when the shutdown ends and what the new data show. If the government reopens before November, the Fed will be able to make a December call based on a real picture of the economy. If the crisis drags on, policymakers will be forced to act almost by feel, and the odds of a pause rise sharply.

For now we can say one thing: the rate is heading down, but there’s no confidence this is the start of a whole series of cuts. The shutdown has turned the U.S. economy into a black box, and the December meeting will be a real test for the Fed.

You can quickly sell or exchange cryptocurrency at a great rate as the Fed rate decision hits—on the time-tested Quickex exchanger.