Decentralized Finance (DeFi) is an open, global financial system built on blockchain technology that eliminates traditional intermediaries like banks and brokerages. By utilizing self-executing smart contracts, users can lend, borrow, trade, and earn interest directly peer-to-peer.

TL;DR:

- Decentralized Finance (DeFi) replaces banks, brokers, and clearinghouses with automated, self-executing software (smart contracts) on a blockchain.

- The system operates 24/7/365, allowing global peer-to-peer lending, borrowing, and trading without requiring identity verification, geographic limits, or credit scores.

- Users retain complete control of their funds through non-custodial wallets rather than depositing capital into a centralized corporate account.

- Financial autonomy comes with severe risks; there is no customer support hotline to reverse transactions, and coding vulnerabilities can lead to permanent loss of capital.

When you look at banking today, it is pretty clear that a lot of the system was built for another era. Traditional banks still rely on centralized structures that are supposed to keep things safe, but they can also hide risk, make cross-border payments slow and expensive, and leave huge numbers of people outside the financial system.

At a deeper level, DeFi feels like the internet’s next big step in finance. Just like the internet disrupted print media and entertainment by removing old middlemen, DeFi tries to do something similar with money and financial services.

That said, it is important to be honest about the downsides. A lot of crypto and DeFi marketing makes the space sound more polished than it really is. In practice, it can feel like the wild west. People say “code is law,” but if the code has a flaw or a bad design, that can mean hackers can steal huge amounts of money, and there is often no way to reverse it.

What we are seeing now is the messy but necessary growth of a new financial system. The first phase was mostly speculation and people experimenting with yield. The next phase, which we are in now, is about the system becoming more mature and useful.

The rise of real-world asset tokenization and faster Layer 2 networks shows this is not just hype. The technology works, and the efficiency gains are real. But until the experience becomes much safer and easier for regular people — especially when it comes to avoiding mistakes like sending money to the wrong address or getting tricked by phishing — DeFi will still feel like a very powerful tool that is hard to use and easy to get burned by.

Defining DeFi: The Shift Toward Financial Autonomy

When you ask what is DeFi, you’re really asking how the internet is upgrading money. For centuries, our financial systems have relied on centralized authorities. If you want a loan, you ask a bank. If you want to trade a stock, you use a broker. These gatekeepers hold your assets, dictate the rules, and extract fees for the privilege of letting you access your own capital.

DeFi meaning at its core is about returning that control to the user. It replaces the banker with mathematics. Instead of corporate servers managing ledgers, a globally distributed network of computers verifies transactions. This shift represents true financial autonomy. You hold the private keys to your digital vault. You interact with autonomous code rather than customer service representatives. This isn’t just an alternative; it’s a structural rebuild of how value moves across the planet.

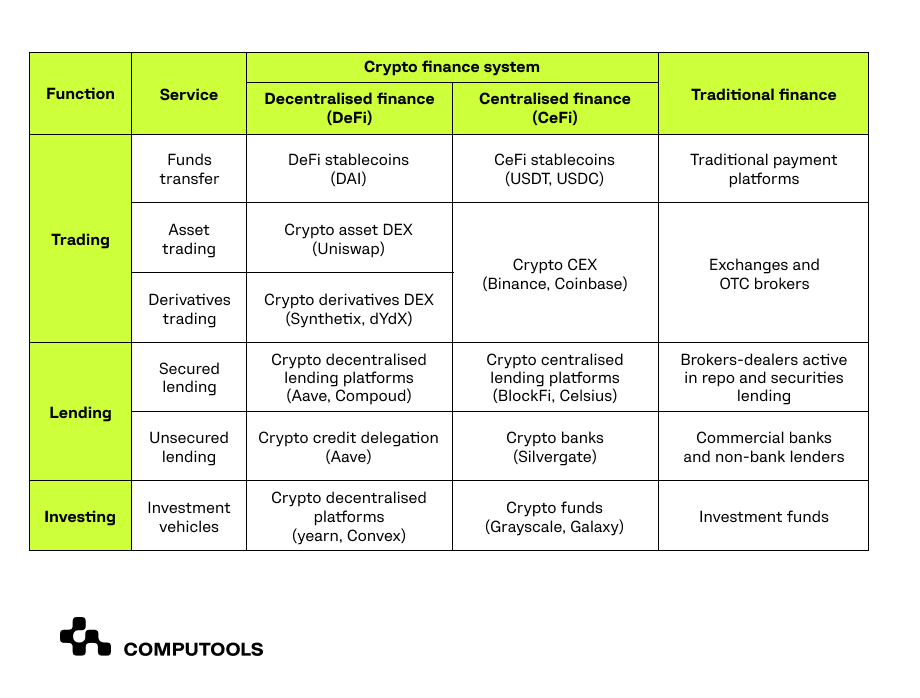

Centralized vs. Decentralized Systems

Source: Computools

To fully grasp whats DeFi, you need to contrast it directly with traditional and centralized structures. Traditional finance operates on local business hours, requires extensive identity verification (KYC), and suffers from prolonged settlement times. Have you ever tried wiring money internationally on a Friday afternoon? It sits in limbo until Monday.

In contrast, what is DeFi in crypto ecosystems? It’s a 24/7/365 machine. Transactions clear in seconds, whether you’re moving ten dollars or ten million. The system doesn’t know your race, credit score, or nationality; it only reads cryptographic signatures. This permissionless nature is the dividing line between legacy banking and the decentralized frontier.

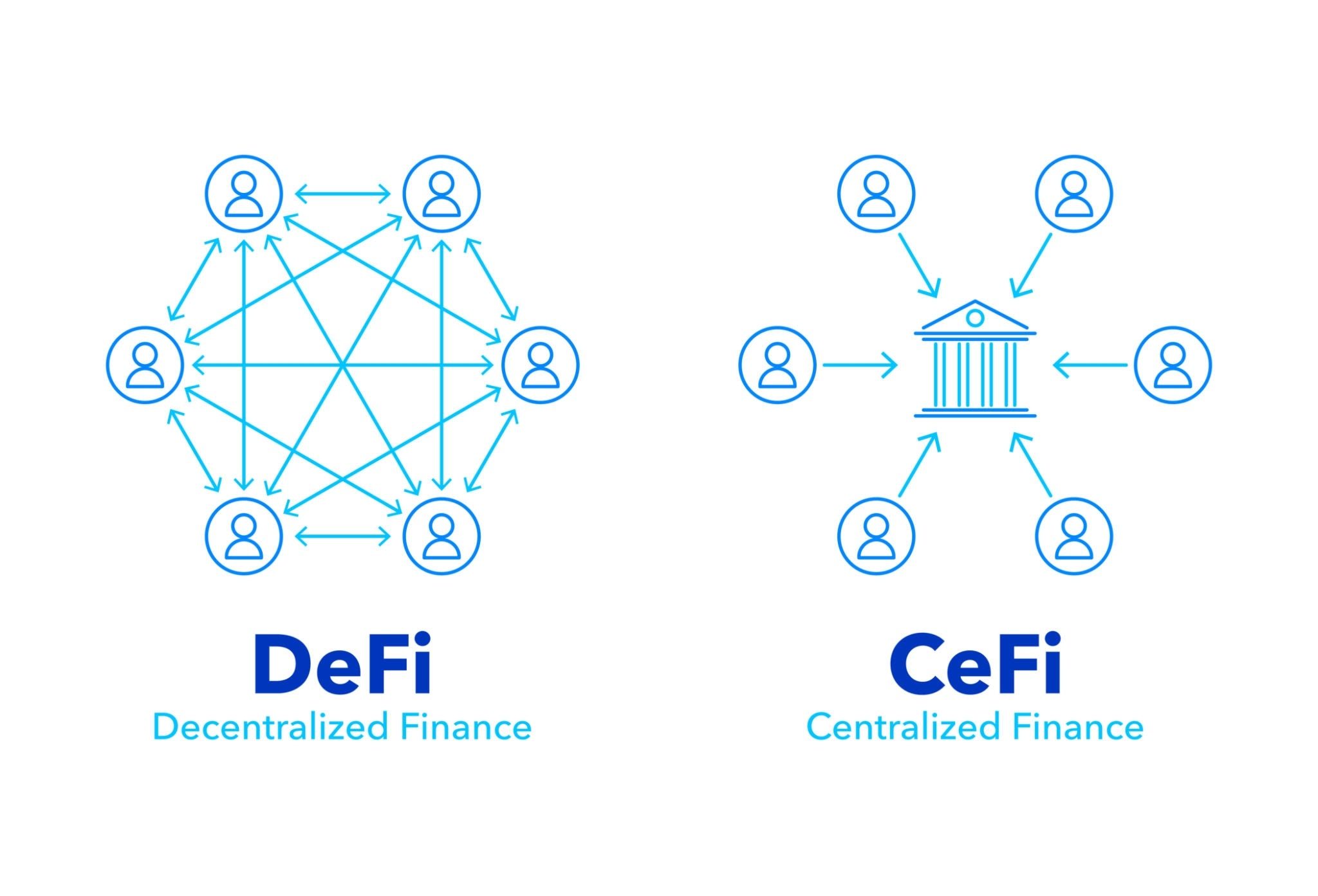

How Does DeFi Work?

Source: Getty Images

Understanding what is DeFi crypto technology is requires peeling back the layers of the network. It’s not a single application, but a stacked architecture of code and cryptography.

The Base Layer

Every decentralized application requires a foundation. This base layer consists of the underlying blockchain—networks like Ethereum or Solana. These networks act as the ultimate source of truth. Thousands of independent computers, known as nodes, constantly communicate to agree on the state of the ledger through consensus mechanisms like Proof-of-Stake. According to ongoing research on the mechanics of financial cryptography published by the International Financial Cryptography Association (IFCA), it is exactly these cryptographic frameworks and distributed consensus models that allow the system to operate securely.

When someone asks crypto DeFi advocates why the system is secure, the answer lies here. No single entity can alter the history of transactions because they would need to overpower a globally distributed network of validators simultaneously.

The Application Layer

If the blockchain is the foundation, smart contracts are the building. A smart contract is simply a piece of code that automatically executes when specific conditions are met. Imagine a vending machine: you insert a coin, select a button, and the machine releases a soda. The transaction happens mechanically without a human clerk.

In the financial realm, smart contracts replace the clearinghouse. If you want to borrow funds, the smart contract automatically assesses your collateral and releases the loan. If your collateral drops below a safe ratio, the contract automatically liquidates it. There is no loan officer to negotiate with; the code is the law.

The Access Gateway

You don’t log into these systems with an email and password. You access them via a non-custodial wallet. This cryptographic software generates a seed phrase—usually 12 to 24 words—that acts as the master key to your digital assets. Because you hold this key, no bank can freeze your account. However, this immense power comes with brutal responsibility. If you lose that phrase, your capital is gone forever. There is no password reset option.

Demystifying the 5 Layers of the DeFi Tech Stack

To truly master the DeFi DeFinition, visualize it as a five-layer cake:

- The Settlement Layer: The base blockchain itself, providing security and finality.

- The Asset Layer: The native coins and issued tokens (like stablecoins) operating on the settlement layer.

- The Protocol Layer: The foundational smart contracts that establish rules for specific activities, like decentralized exchanges or lending markets.

- The Application Layer: The user interface (UI) built on top of the protocols. This is the website you actually interact with.

- The Aggregation Layer: Platforms that pull data and liquidity from multiple applications to find users the best possible rates or yield farming opportunities.

The Primary Use Cases of DeFi

Now that we know the architecture, what can you actually do with it?

Decentralized Lending and Borrowing Protocols

Traditional banks take your deposits, lend them out at high interest, and pay you a fraction of a percent. Decentralized lending removes the bank entirely. Users deposit their digital assets into a global smart contract “pool.” Borrowers can then pull from that pool by providing over-collateralized assets as security. The interest paid by the borrower goes directly to the depositor. It’s a pool-to-peer system that operates with ruthless efficiency.

Decentralized Exchanges and Automated Market Makers

A cornerstone of what is decentralized finance is the ability to trade without a broker. Traditional exchanges use order books—matching buyers with sellers. Decentralized Exchanges (DEXs) use Automated Market Makers (AMMs). Instead of waiting for a human counterparty, you trade directly against a liquidity pool controlled by an algorithm. The algorithm automatically adjusts the price of the asset based on the ratio of tokens left in the pool. It ensures there is always a buyer and a seller, no matter how volatile the market gets.

Liquidity Pools, Yield Farming, and Staking Mechanics

Because AMMs need capital to function, they incentivize users to provide it. By depositing a pair of assets into a liquidity pool, you become a market maker. In return, the protocol pays you a share of the trading fees generated by that pool. This process of hunting for the highest return on deposited capital is known as yield farming. Staking works similarly, but usually involves locking up a native token to help secure the base blockchain itself in exchange for inflationary rewards.

Programmable Money: Stablecoins and Tokenization

You can’t build a reliable financial system if the unit of account swings wildly in value every hour. Enter stablecoins. These are digital assets mathematically or physically pegged to a fiat currency, usually the US Dollar. They are the essential transactional grease of the ecosystem. They allow traders to lock in profits and lend out capital without worrying about market volatility.

Decentralized Governance

Who runs these protocols? Decentralized Autonomous Organizations (DAOs). Instead of a board of directors sitting in a corporate office, a protocol is governed by the people who hold its governance tokens. 1 token equals 1 vote. The community proposes upgrades, votes on fee structures, and decides how to spend the protocol’s treasury.

As detailed in the comprehensive analysis DeFi Beyond the Hype by the Wharton Blockchain and Digital Asset Project, these token-weighted voting structures represent a profound shift in autonomous governance, effectively replacing traditional corporate hierarchies with internet-native democratic experiments.

Prediction Markets, Web3 Insurance, and GameFi

The ecosystem is expanding rapidly beyond basic lending. Prediction markets, like Polymarket, allow users to wager on real-world events using cryptographic truth. Web3 insurance protocols allow users to pool funds to cover smart contract failures. GameFi integrates financial mechanics directly into video games, allowing players to truly own their in-game assets and earn yields simply by participating in digital economies.

Evaluating Traditional vs. DeFi Capital Mechanics

Reading about DeFi crypto meaning is one thing; seeing the math in action is another. Use the interactive calculator below to compare the actual growth, fee structures, and execution times between traditional savings accounts and decentralized yield protocols.

Case Studies: Blue-Chip DeFi Protocols in Action

To anchor our understanding of what does DeFi mean, we must look at the giants that survived multiple market cycles and continue to secure billions in value.

Uniswap: Redefining Token Swaps via On-Chain Liquidity

Uniswap is the undisputed king of Decentralized Exchanges. It popularized the AMM model using a simple yet brilliant mathematical formula: X x Y = K. In this equation, X and Y represent the quantity of two tokens in a liquidity pool, and K is a constant total. When a trader buys one token, they add the other to the pool, automatically driving up the price of the purchased token to maintain the constant. This elegant code eliminated the need for traditional market makers entirely.

Aave: The Leading Non-Custodial Liquidity Market

Aave operates as the central bank of the decentralized world. It pioneered the concept of flash loans—uncollateralized loans that must be borrowed and repaid within the exact same blockchain transaction block. If the loan isn’t repaid instantly, the entire transaction simply reverses as if it never happened. This allows developers to execute massive arbitrage opportunities with zero initial capital, showcasing the sheer programmable power of smart contracts.

MakerDAO: Scaling the Decentralized Dollar (DAI)

MakerDAO is the engine behind DAI, a decentralized stablecoin. Unlike centralized stablecoins that hold physical dollars in a traditional bank vault, DAI is generated by users locking up volatile crypto assets as collateral into Maker’s smart contracts. If the value of that collateral drops too close to the value of the minted DAI, the protocol automatically liquidates the collateral to ensure DAI always remains backed and pegged to the dollar.

The Critical Risks and Disadvantages of DeFi

For all its revolutionary potential, this frontier is inherently dangerous. Anyone explaining what is the DeFi landscape without mentioning the risks is selling you a fantasy.

Technical Vulnerabilities

Because the system runs on open-source code, that code is entirely visible to hackers. If a developer makes a logic error, a hacker will find it. Millions of dollars can be drained in seconds through re-entrancy attacks or flash loan manipulation. Furthermore, smart contracts rely on “oracles” to feed them real-world price data. If an oracle is manipulated to report the wrong price, the smart contract will execute flawlessly based on that bad data, leading to catastrophic liquidations.

Economic Dangers

The crypto markets are notoriously volatile. If you borrow against your assets and the market crashes, the smart contract will mercilessly liquidate your holdings to protect the lenders. There are no margin calls or grace periods.

Additionally, liquidity providers face “impermanent loss.” This occurs when the price ratio of the tokens you deposited into an AMM changes significantly from when you deposited them. You would have been better off simply holding the tokens in your wallet rather than providing them as liquidity.

Human Friction

You are your own bank. That sounds empowering until you send funds to the wrong network address. Blockchain transactions are immutable. If you make a typo, there is no centralized authority to reverse the transaction. If you write down your seed phrase incorrectly, your funds are permanently locked behind cryptography that the world’s most powerful supercomputers cannot break.

The Dark Side: Regulatory Scrutiny, Rug Pulls, and Phishing Scams

The permissionless nature of the network means anyone can create a token and list it on a DEX. Malicious developers frequently create hype around a fake project, wait for users to pour capital into the liquidity pool, and then drain the pool—a maneuver known as a “rug pull.” Furthermore, phishing attacks are rampant. Signing a malicious smart contract approval can give a hacker full permission to drain your wallet instantly.

How to Safely Participate in DeFi: A Step-by-Step Guide

If you are ready to explore what is DeFi?, you must approach it methodically. Safety must be your primary baseline.

- Vetting and Selecting a Secure Web3 Wallet (Hardware vs. Software): Start by downloading a reputable browser extension wallet. However, if you are moving significant capital, you must invest in a hardware wallet. These physical devices keep your private keys completely offline, immunizing you from malware and keyloggers.

- Sourcing Native Crypto-Assets Safely via Regulated Centralized Exchanges (CEXs): You cannot enter a decentralized network without “gas” money to pay for network transactions. Purchase your initial base-layer tokens (like ETH to BTC) on a regulated, centralized exchange, and then withdraw them to your private Web3 wallet.

- Connecting Wallets to On-Chain Applications and Managing Approvals: When you visit a decentralized application, you will connect your wallet. Read every prompt carefully. You are signing digital contracts. Never approve unlimited token spending unless you are interacting with a heavily audited, blue-chip protocol.

- Interpreting On-Chain Gas Fees and Network Speeds Before Execution: Before finalizing a transaction, the wallet will estimate your network fee (gas). During times of heavy congestion, these fees can spike dramatically. Learn to read network scanners to time your transactions during off-peak hours.

- Essential Portfolio Habits: Revoking Permissions and Diversifying Across Networks: Your digital hygiene matters. Use token allowance checkers regularly to revoke smart contract permissions you no longer need. Never put all your capital into a single protocol. Diversify across different base layer blockchains to mitigate systemic risk.

Future Trends and Institutional Integration

The ecosystem of 2026 looks vastly different from its origins. We are moving from pure retail speculation into heavy infrastructure.

Real-World Asset (RWA) Tokenization

The next trillion dollars will not come from native digital tokens; it will come from Real-World Assets. We are actively seeing US Treasuries, private real estate equity, and commodities tokenized and brought on-chain. This allows for fractional ownership, instant global settlement, and using physical real estate as collateral in digital lending markets. It bridges the gap between traditional yield and decentralized liquidity.

Scaling Solutions

The biggest historical criticism of the network was its inability to handle high transaction volumes without massive fees. Layer 2 networks solved this. By processing thousands of transactions off the main chain and rolling them up into a single cryptographic proof, they have reduced fees to fractions of a cent while maintaining base layer security. Cross-chain bridges are now seamlessly connecting these separate networks, creating a unified, multi-chain financial fabric.

The Rise of Regulatory-Compliant DeFi

Institutions want the efficiency of smart contracts, but they cannot legally interact with anonymous wallets. The Bank for International Settlements (BIS) has repeatedly emphasized in its working papers that addressing systemic risk and regulatory compliance is mandatory before legacy capital can merge with decentralized architecture.

The solution is permissioned liquidity pools. These are walled gardens where every participant has passed stringent KYC checks. It represents a hybrid approach: the speed and transparency of decentralized architecture wrapped in traditional regulatory compliance.

Is DeFi Right for Your Financial Portfolio?

Decentralized finance is not a fad; it is a permanent restructuring of how humans transfer value. By removing the rent-seeking middlemen, it offers unprecedented transparency, immediate settlement, and globally accessible yield.

However, it is a frontier that demands relentless personal responsibility. There are no safety nets, and the learning curve is steep. If you are willing to study the mechanics, secure your private keys, and manage your risk, participating in this ecosystem offers a front-row seat to the future of the internet economy.

Frequently Asked Questions About DeFi

Can you make real money with DeFi?

Yes. By providing liquidity or lending assets, users capture the fees that traditionally went to bankers and brokers. However, yields are directly proportional to risk. A 5% stablecoin yield is generally considered safe, while a 50% yield on an unproven token is a massive red flag that carries severe smart contract and volatility risks.

Is DeFi safe for long-term retirement investing?

It depends entirely on your risk tolerance and technical competence. While blue-chip protocols have operated flawlessly for years, the broader ecosystem is still nascent and highly experimental. It should only represent a calculated, high-risk portion of a broadly diversified portfolio, not your entire retirement nest egg.

What is the fundamental difference between traditional crypto and DeFi?

Traditional crypto often involves simply buying a digital asset on a centralized exchange and hoping the price goes up. Decentralized finance represents the active deployment of those assets using self-executing smart contracts to generate productive yield, borrow capital, and trade synthetics without a middleman.

Do I have to pay capital gains taxes on my DeFi earnings?

In almost all major jurisdictions, yes. Tax authorities view crypto-to-crypto swaps, earning liquidity pool rewards, and staking yields as taxable events. You are responsible for tracking your on-chain history using specialized crypto tax software to ensure compliance.

What does Total Value Locked (TVL) mean in crypto analytics?

Total Value Locked represents the dollar amount of assets currently deposited into a specific protocol’s smart contracts. It is the primary metric used to gauge the health, trust, and liquidity of a decentralized application.